Business is nothing but a chain of activities involving capital, labor, and innovation to produce goods and services. One such vital aspect of holistic business operation is – the movement of goods to the intended stakeholders.

There are different stages of business operations that rely on diverse sources of input and output resources. So, in accounting, the cost of shipping or handling goods is categorized into two segments: carriage inwards and carriage outwards.

Today, we will talk about the carriage inward meaning, its accounting application, and the basic differences between carriage inwards and carriage outwards.

What is Carriage Inward?

Carriage Inward is the cost incurred during transit of the goods or assets purchased. It constitutes all the expenses obtained while transporting goods. When the buyer makes purchases of capital assets, raw materials, or inventory, they need to be consigned to the intended locations, such as warehouses or business areas, for further operations.

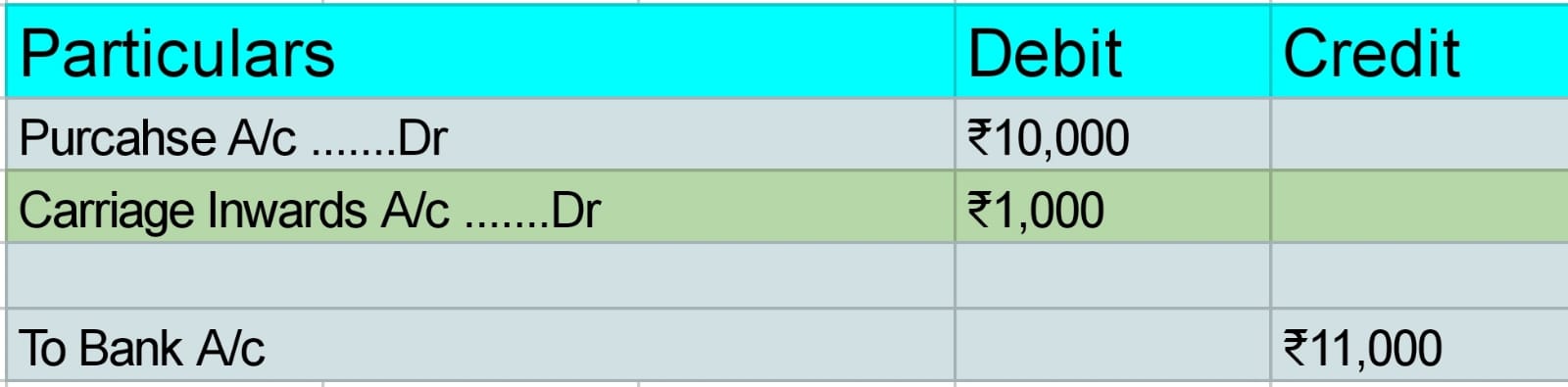

Let’s see an example of a carriage inwards journal record.

A company purchases goods worth ₹10,000 and pays an additional ₹1,000 as freight inwards, i.e., cost of transportation.

(Being carriage inwards paid while purchasing goods)

Accounting Treatment of Carriage Inwards

In the books of account, freight inward is treated as a direct expense and included in the cost of purchased goods. We display it on the debit side of the trading account. The buyer is liable to pay all such expenses related to transit.

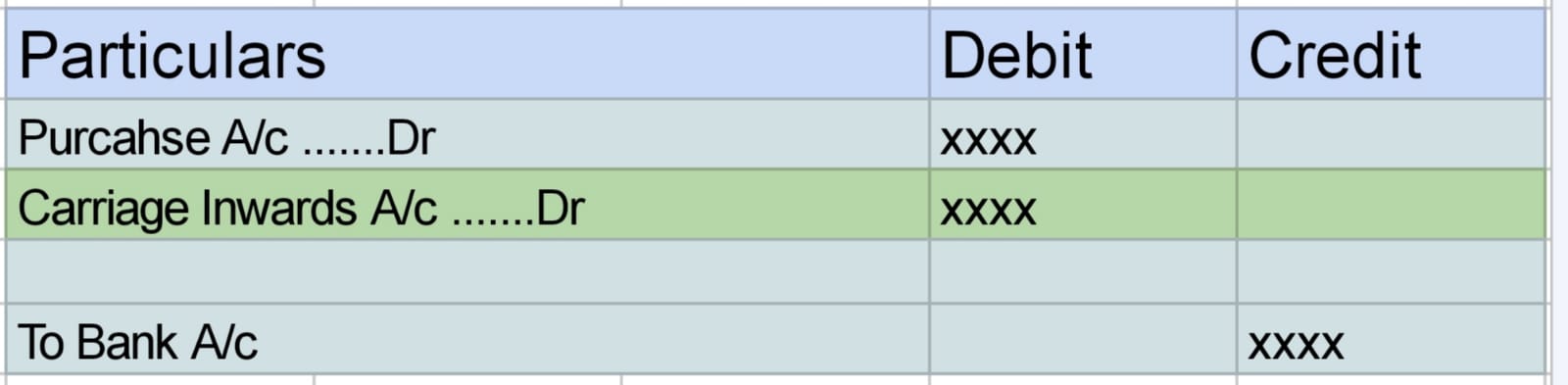

Journal Entry: Purchasing Goods

Carriage inwards in trading account shown on the debit side, while purchasing inventory or goods.

(Being carriage inwards paid while purchasing inventory)

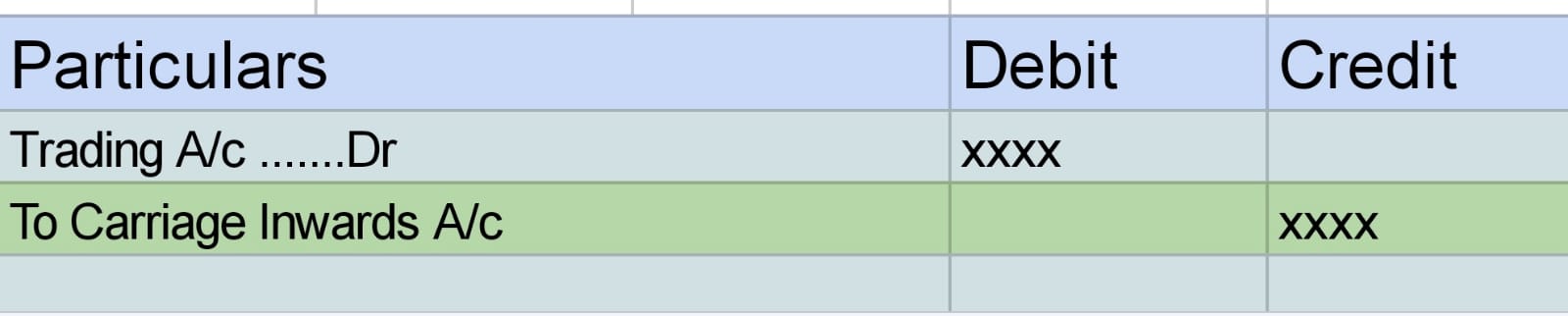

The next step is transferring freight inwards to the trading account. The buyer may add value to the COGS (Cost of goods sold).

(Transferring of carriage inwards to the trading account)

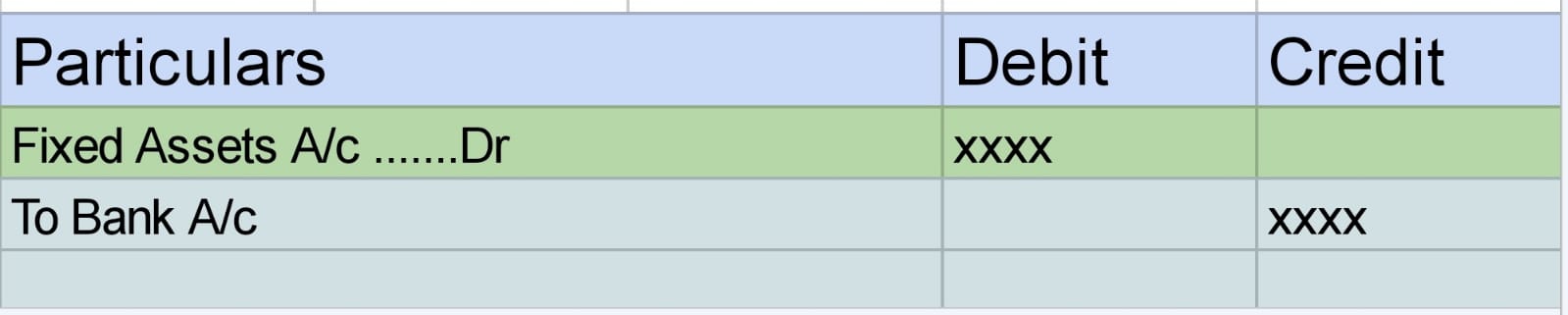

Journal Entry When Purchasing Fixed Assets

When purchasing a fixed asset, carriage inwards is treated as a part of capital expenditure. Here, the shipment costs are added to the overall cost of the fixed asset.

(Carriage inwards is paid inclusively with the purchase of a fixed asset)

Differences between Carriage Inwards and Carriage Outwards

Popularly, there are two types of transit expenses – carriage inwards and carriage outwards. One represents the expense of procuring goods or assets from the supplier, whereas, the other denotes the transportation charges of selling goods to the customers.

We have learned about freight inward meaning and its accounting treatment. Let’s find out the meaning and its accounting application.

Carriage Inwards vs. Carriage Outwards

Carriage outward and carriage inward in trial balance are shown on the debit side, as both are recorded as expenses. There are some fundamental differences as well. We will look into these distinctions and their application in the books of accounts.

Here is a comprehensive table detailing the differences between carriage inwards and carriage outwards:

|

Basis

|

Carriage Inwards

|

Carriage Outwards

|

|---|---|---|

|

Meaning

|

Expenses incurred for transit/freight while purchasing goods.

|

Charges incurred for transportation/freight while selling or delivering the goods.

|

|

Borne By

|

The buyer bears it most of the time while purchasing the goods.

|

The seller or buyer of the goods bears the expense, as per the terms of the sale.

|

|

Type of cost

|

It is a direct expense and forms part of total goods costs for the purchaser or buyer.

|

It is an indirect expense and forms the part of selling and distribution costs for the seller.

|

|

Accounting Treatment

|

Carriage inward is shown on the debit side in the books of trading accounts.

|

Carriage outwards comes under the debit side in the books of the profit-and-loss account.

|

|

Capitalization

|

Capitalized only when a fixed asset is purchased.

|

It is a revenue cost and is never capitalized.

|

|

Other Names

|

Freight inward, freight in or transportation inward

|

Freight inward, freight in or transportation inward

|

Conclusion

Transportation of goods is a vital aspect of business operation. Carriage inwards is a transit cost paid by the buyer of the goods. It is associated with the process of buying goods or raw materials and making finished products. Hence, all the expenses are included in the calculation cost of goods sold.

If a business is purchasing a fixed asset, it will include the expenses in the overall cost of the acquisition.

Mostly, buyers are liable for the cost of carriage inwards. However, in rare cases, the transportation cost is split between buyer and seller as per the sale agreement. It is essential to record transportation costs appropriately in the books of buyers and sellers for better understanding.