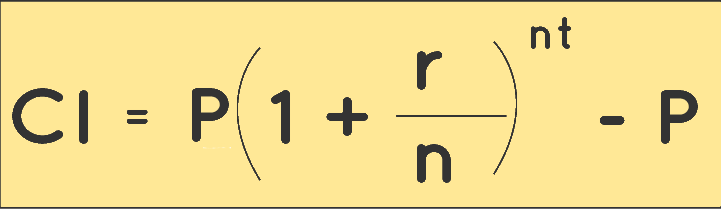

The interest that is calculated on both principal and previous interest and is compounded on a regular basis is known as compound interest. The interest is computed on a new principal every time. This principle is the cumulation of the accrued interest and the original principal.

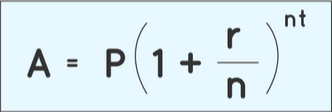

The formula for calculating the amount:

Compound interest can be calculated annually, semi-annually, quarterly, or even monthly. This is similar to how reinvested interest in an investment accelerates the growth of the principal over time. It is exactly what money does due to compound interest. Banks and other financial institutions only calculate the amount using compound interest.

The total amount at the conclusion of the time period, which includes the principle and compound interest, is represented by the formula above. Moreover, by deducting the principal from this sum, we can get the compound interest.

To compute compound interest: