Introduction

In today’s time, everybody who has a bank account have seen and used cheques and they play an important part whenever you need to transact money from these bank accounts.

A cheque is a fundamentally important document that an individual, company and others use to withdraw or transfer money. There are various types of cheques available in our banking sector which have different requirements. So, let’s learn more about types of cheques.

What is a cheque?

A cheque is a document/paper which orders the bank to transfer money from the bank account of an individual or an organisation to another bank account.

A cheque is a common form of a negotiable instrument. You need to have a savings bank account or current account in a bank, in order to issue a cheque in your own name or in favour of other parties, thereby ordering the bank to pay the said amount to whoever named in the cheque. It is one of the safest and convenient modes of payment transfers and you can transfer a high-value transaction without any hassle which would be very difficult if hard cash was used instead. This transaction needs to be handled very delicately as it can lead to some serious banking fraud.

Parties to a cheque

The parties that are involved with a cheque are:

Payee: The person named in the cheque who is to receive the payment

Drawee: The specific bank on which the cheque has been drawn

Drawer: The person who writes the cheque, who can be the account holder or the customer. The payee and drawer can be the same person.

Endorser: When the right to take the payment is transferred by the payee to another party, the payee is called an endorser.

Endorsee: When the right to take the payment is transferred by the payee to another party, the party to which the right is transferred is called the endorsee.

Features of a cheque

Cheques can be issued against savings or current accounts

- A cheque is always drawn on a specified banker

- It is an unconditional order

- The payee of a cheque is fixed and certain and cannot be changed

- The payment will only be made in the name of the payee/beneficiary

- It is an instrument that is payable on demand

· A cheque will be considered invalid if does not contain the date

Types of cheques

Open cheque

An open cheque is a kind of leaf that a bank account holder can use to order the bank to make a payment to another party or deposit in his very own account.

Bearer cheque

In a bearer cheque, the money is made to a person who’s appearing on behalf of the payee/beneficiary, in whose name the cheque has been issued. In the leaf, it is a must to include the word ‘bearer’ in this kind of cheque.

Self-Cheques

A self-cheque is a cheque drawn in one’s very own call, because of this that the drawer and the payee are the same. You might write the word ‘’self’’ in the area for the drawee’s call at the cheque. It can simplest be encashed in the drawer’s financial institution. A self-cheque is to be used in conditions while you need to withdraw cash out of your very own account. It must be considered if one of these cheque falls in incorrect hands, it could be misused by any man or woman to withdraw cash from the financial institution from which the cheque is issued, so a self-cheque ought to be stored safely.

Account Payee Cheques

An account payee cheque is a bearer’s cheque that has the words ‘’account payee’’ written at the top left-hand side, within parallel lines, and crossed twice. This is also called a ‘’crossed cheque’’. It is the most secure way to issue a cheque as the amount written can be transferred only to that specific person’s account.

Post-dated cheque

A post-dated cheque is an account payee or crossed cheque that has a future date with a purpose to meet a financial obligation in future. It is legitimate for up to a few months from the date of the cheque’s issuance.

Banker’s cheque

Banker’s cheques are cheques which are issued by the bank so it guarantees payment.

Traveler’s Cheque

A traveler’s cheque is used when travelling as it is difficult to carry cash and coins and it is a more secure way. It may be encashed while travelling overseas wherein overseas forex is required.

Stale Cheque

A cheque in India is valid for 3 months from the date of issue. Any cheque which has been deposited three months after the date of the cheque being signed becomes a stale cheque.

Blank Cheque

A cheque which has all the fields blank except for the drawer’s signature, then it is called a blank cheque.

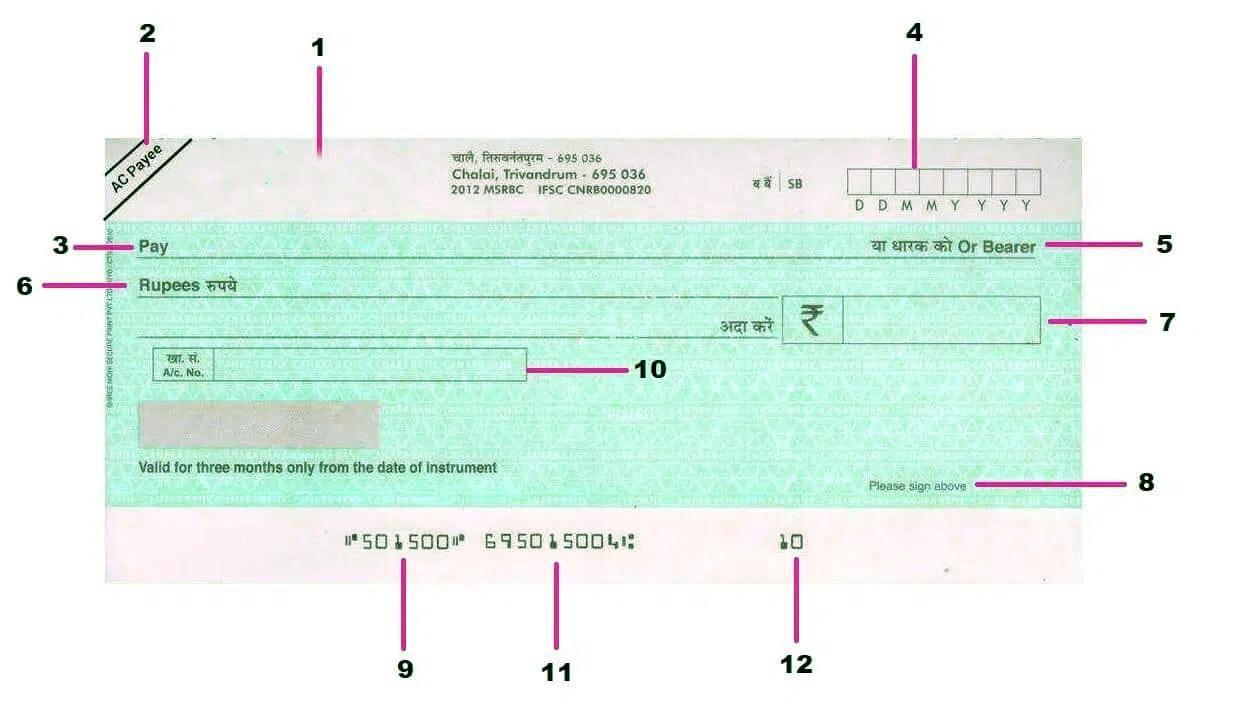

Various parts of the cheque

One needs to understand the different elements of the cheque to make sure that the cheque is written correctly. Here are some of the essential parts of the cheque-

- Name of the bank is also called the drawee bank or payee bank

- If there is a crossing on it and written a/c payee only, it is a directive to the bank to pay in the account of payee only.

- In the pay section, you need to mention the name of the payee for whom you are making the cheque. Make sure that the name is spelt correctly. It is advised to draw a line on the space after writing the payee’s name so that no changes can be made.

- In the date section, mention the date on which you want the money to be debited or transferred.

- You should always cross the or bearer option so that if the cheque is stolen, it cannot be paid.

- Mention the amount in words here and draw a line after it is mentioned. Write the amount close to the bank. Also, ensure that the amount written in words and numbers are the same as if they do not match then the cheque can return.

- Make sure to write the amount in numbers and to draw a line after the amount so no one can make changes.

- Do your authorised signature as a drawer.

- Every cheque has a different serial number. It is called Cheque Number.

- Account number of the cheque issue is mentioned here.

- MICR code is the Magnetic Link Character Recognition Code. It indicates the bank and branch from where the cheque is issued.

- 12. These two digits are the transaction ID.

Conclusion

Cheques are one of the most convenient and easy ways to transfer money. There are various types of cheques that can be useful to withdraw money from your bank account as and when required.