One thing that holds utmost significance in accounting and finance is the net wort – how much the company owns and how much it owes. It is also called the book value of a company. The most prominent way to know how much a company values, the balance sheet is the key. A balance sheet includes all the assets and liabilities of a company along with the equity proportion of shareholders. Reading a balance sheet may appear challenging, but anyone can perform this task with some basics cleared.

This article will help you understand what a balance sheet is, what a consolidated balance sheet is, and why it is crucial for any business with an example.

What is a balance sheet in accounting?

A business has to prepare three financial statements, and a balance sheet is one of them. A balance sheet represents the total assets, the sources of assets, whether equity or debt, total liabilities, and the shareholders’ equity. As a result, it is also called the statement of financial position.

The balance sheet of a company contains two sides, where the left section has the total assets of a company and the right side contains the total liabilities and Shareholders’ Equity.

This can be stated as the balance sheet equation = Total Assets = Total Liabilities + Total Equity

Apart from the border classifications of assets and liabilities, these two are further divided into more categories – current and non-current assets and liabilities.

A balance sheet helps a company find key ratios such as current ratio, liquidity ratio, debt to equity ratio, etc. This helps the internal and external stakeholders and investors know how viable the business is. Important decisions on the company policy, business strategy, financing, etc., are taken based on the balance sheet numbers. The balance sheet for a company is typically created every quarter as well as on an annual basis. Though some companies also prefer to make it on a monthly basis.

What is a consolidated balance sheet?

Now that the basis for the balance sheet is clear, let us get into a little more detail. The concern to create a consolidated balance sheet arises when a company owns a subsidiary of other companies—for example, Alphabet and Google. Alphabet is the parent company, and Google is its subsidiary. If a company owns more than 50 percent stake in another company, it can choose to make a consolidated balance sheet.

In a consolidated balance sheet, the assets and liabilities of the subsidiaries are also included in the parent company’s assets and liabilities without any distinctions.

It is an easy task if the parent company has a 100 percent stake in the subsidiary. However, suppose the stake is less than that. In that case, the ideal accounting method is to include the subsidy’s assets and liabilities to the parent company’s particulars and create a separate head of Non-controlling Interest or Minority Interest under Shareholders’ Equity. It balances both sides.

Balance sheet format

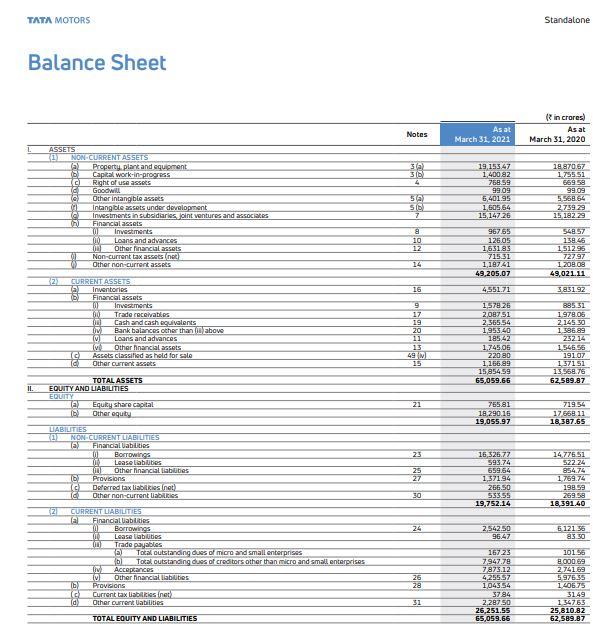

Below is the standalone balance sheet of TATA Motors for FY 2020-21.

Let’s understand the line particulars in detail.

Non-current Assets

The major particulates for this tab are as follows.

- Plant, Property, and Equipment (PP&E): All the tangible assets of a company are included under this heading. All the assets except land are added to a net of depreciation in the balance sheet of a company.

- Intangible Assets: Assets such as licenses, patents, etc., cannot be seen but holds value. They are included under the tag of intangible assets.

Current Assets

Current Assets are divided into three major categories.

- Cash and Cash Equivalents: This includes all the liquid and short-term assets a company owns. They typically have less than three months of maturity. More details on the equivalent are always mentioned in the footnote of the balance sheet.

- Accounts Receivable: This includes all the total revenue that is yet to come. Any bad debt expenses are deducted from receivables. When a company receives a credit from a doubtful account, it is added to the cash and is deducted from receivables.

- Inventory: This tab includes the sum of raw materials, work in progress (WIP), and finished goods and services.

Non-Current Liabilities

The primary line items under this tab are as follows.

- Long Term Debt: A company showcases its total Long Term Debt excluding the part of current Non-Current Debt under this tab. It is typically classified as per different payable schedules and includes details of interest amount and principle for each maturity period.

- Bonds: This tab included the amortization sum of bonds issued by the company.

Current Liabilities

Current Liabilities can be divided into three parts.

- Accounts Payable: This is the opposite of Accounts Receivable, as in, the company is yet to pay the due to suppliers. When the company pays out the due, the cash account is reduced along with the payables account for the same sum.

- Current Debt or Debts Payable: Any item excluded from Accounts Payable is included under this tab. Current Debt usually has a time frame of a year or less than a year. Sometimes it also includes Notes Payable for longer than a year.

- Current Long Term Debt: It is at the discretion of a company to add Long Term Debt to the Current Debt or show it separately. Long Term Debt has a longer maturity, typically of more than a year.

Shareholders' Equity

Shareholders’ Equity contains two parts.

- Equity Share Capital: Shareholders fuel the cash demand when a company starts. The cash part is included under current assets, while to balance it out, the same is added to the Shareholders’ Equity. This is the total sum that shareholders of a company have put in for the growth.

- Retained Earnings: The total net profit mentioned in the income statement is added to the balance sheet under the tag of Retained Earnings. This is the sum that the company has left with after paying dividends to shareholders (if any).

Conclusion

A balance sheet is a crucial element to understanding a company’s financial position. The most useful purpose that it serves is bifurcating how the company has sourced its finances. A balance sheet also helps in getting critical financial ratios that allow comparison between competitors and different time points to take actions accordingly and grow.