Two essential measurements generally used in the investing and financial world are Hurdle Rate and Internal Rate of Return (IRR). Both of them are used for varying purposes. But there seems to be no end to the confusion they’ve caused among newcomers. So, if you cannot differentiate between hurdle rate and Internal Rate of Return (IRR), this post is meant to give you clarity. Let’s find out more about hurdle rate vs Internal Rate of Return here.

Know The Difference Between Hurdle Rate Vs Internal Rate Of Return

What is Hurdle Rate?

Also known as the minimum acceptable rate of return, the hurdle rate is the lowest rate of return that an investment or a project must earn to offset the investment’s costs. Projects are also assessed by discounting future cash flows to the current hurdle rate to calculate the Net Present Value (NPV).

This, in turn, showcases the difference between the current value of cash outflows and the current value of cash inflows. Usually, the hurdle rate is equal to a company’s capital costs, which is the amalgamation of the cost of debt and the cost of equity.

Typically, managers raise the hurdle rate either for such projects that are riskier or when the company is comparing several investment opportunities.

Understanding Hurdle Rate

This metric describes an adequate compensation for the current risk level. The hurdle rate lets companies make vital decisions on whether to pursue a specific project or not. If the anticipated rate of return goes above the hurdle rate, the investment is regarded as sound. If it goes below the hurdle rate, the investment is considered riskier.

To determine the hurdle rate, some of the essential areas that should be considered are:

- Associated risks

- Cost of capital

- Returns of other potential projects or investments

Hurdle Rate Formula

To calculate the hurdle rate, here is the hurdle rate formula that can be used:

Hurdle rate = Cost of Capital + Risk Premium

Hurdle Rate Example

Let’s consider an example to understand more about hurdle rate. Suppose you are looking forward to buying new machinery. As per the evaluation, with this new machine, you can increase the sales of your product, resulting in a return of almost 11% on the investment.

The Weighted average cost of capital (WACC) for your company is 5%. The risk of not selling additional products is low. Thus, a low-risk premium got assigned at 3%.

Then, the hurdle rate will be:

5% (WACC) + 3% (Risk premium) = 8%

Since the expected return on this investment is 11% and the hurdle rate is 8%, which is lower, buying the new machine will be a sound investment for you.

Read About – Exponential Growth

What is the Internal Rate of Return?

The Internal Rate of Return (IRR) is the anticipated annual amount of money (expressed in percentage) that an investment is expected to generate for a company above and over the hurdle rate.

The word “internal” denotes that the figure doesn’t account for possible external factors and risks, such as inflation. Also, IRR is used by financial experts and professionals to evaluate the expected returns on several stocks and investments, such as the yield to maturity on bonds.

Understanding IRR (Internal Rate Of Return)

Basically, the Internal Rate of Return (IRR) is one such discount rate that makes a project’s Net Present Value (NPV) zero. In simple words, it is the anticipated compound annual rate of return that will be earned on an investment or a project.

You can only use IRR when looking at investments and projects with an initial cash outflow and one or more inflows. Moreover, this method doesn’t consider the possibility that various projects may have varying durations.

While it is comparatively straightforward to assess projects by comparing the IRR to the hurdle rate, this approach has specific limitations in the form of an investing strategy.

For example, it considers only the rate of return, in contrast to the return’s size. A $10 investment returning $100 has a higher rate of return than a $10 million investment yielding $2 million.

Once you’ve determined the internal rate of return, it is generally compared to the cost of capital or a company’s hurdle rate. If the IRR equals or exceeds the cost of capital, the company will accept the project as a sound investment. And, if the IRR is lower than the hurdle rate, it will be rejected.

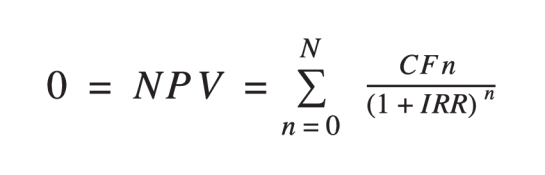

IRR Formula

The IRR formula is as mentioned below:

Here,

NPV = Net Present Value

N = Holding Period

n = Each Period

CF = Cash Flow

IRR = Internal Rate of Return

One can do the calculation of the internal rate of return in three varying methods:

- Using the XIRR or IRR function in a spreadsheet or Excel programs

- Through an iterative process where an analyst tries a variety of discount rates until the NPV is equal to zero

- Through a financial calculator

IRR Example

Before moving ahead with understanding IRR, you’ll first have to know Net Present Value (NPV). This is because the cash that you have today is far more valuable than the one you’ll get after five years, courtesy of inflation. Thus, when you think of investing money every year, you must first check its worth today.

So, let’s assume you invested Rs. 10 lakhs in a project X today. From the next year, this project will start making cash flows without the need for further investments. You can find more information on the money that you’ve invested today and the cash flows that it will generate in the future in the below-mentioned table.

Time Period (Years) | Cash Flow |

Today | Rs. – 10 lakhs |

Year 1 | Rs. 2 lakhs |

Year 2 | Rs. 3 lakhs |

Year 3 | Rs. 3 lakhs |

Year 4 | Rs. 3.5 lakhs |

Year 5 | Rs. 3.5 lakhs |

Total Cash flow | Rs. 15 lakhs |

Now, to find out NPV of the cash flows mentioned above, suppose IRR is approximately 8% for the project X. discount every cash flow with IRR while considering the time lapse. The NPV formula is:

NPV = Cash Flow / Discount Rate + 1^N.

Here,

N = number of years

Time Period | Project X | Discount Rate | NPV (Rs) |

Today | Rs. – 10 lakhs | 8% | (10 lakhs) |

Year 1 | Rs. 2 lakhs | 8% | 1,85,185 |

Year 2 | Rs. 3 lakhs | 8% | 2,57,202 |

Year 3 | Rs. 3 lakhs | 8% | 2,38,150 |

Year 4 | Rs. 3.5 lakhs | 8% | 2,57,260 |

Year 5 | Rs. 3.5 lakhs | 8% | 2,38,204 |

Total cash flows | 11,76,001 |

The table mentioned above displays that Project X has NPV worth Rs. 11.76 lakhs. And you’re investing Rs. 10 lakhs today. This simply shows that this project isn’t worth investing as you’ll only get the benefit of Rs. 1.76 lakhs after five years.

NPV should be more than zero, which means the project should give more returns than the money you’re investing today.

In the example above, if you replace put 13.92% in the place of 8%, the NPV will turn zero and that will be your IRR. Thus, IRR can be defied as the discount rate at which a project’s NPV becomes zero.

Time Period | Project X | Discount Rate | NPV (Rs) |

Today | Rs. – 10 lakhs | 13.92% | (10 lakhs) |

Year 1 | Rs. 2 lakhs | 13.92% | 1,75,569 |

Year 2 | Rs. 3 lakhs | 13.92% | 2,31, 184 |

Year 3 | Rs. 3 lakhs | 13.92% | 2,02,944 |

Year 4 | Rs. 3.5 lakhs | 13.92% | 2,07,846 |

Year 5 | Rs. 3.5 lakhs | 13.92% | 1,82,457 |

Total cash flows | 10 lakhs |

Calculating IRR

- In an excel sheet, enter the original invested amount, make sure you put a minus (-) sign in front of the amount

- In every cell, enter the cash flows received in the respective year

- Add minus (-) whenever you’re investing money

- Find IRR by entering =IRR(values,guess)

Number of Years | Project X |

Today | -1000000 |

Year 1 | 200000 |

Year 2 | 300000 |

Year 3 | 300000 |

Year 4 | 350000 |

Year 5 | 350000 |

IRR | 14% |

Final Thoughts

By now, it would be clear that both of the metrics – hurdle rate and Internal Rate of Return – are essential. In a corporation, both play an integral role in deciding whether an investment or a project will be worthwhile. If running a company, you must understand these concepts thoroughly and ensure their application is helping you achieve the best results.